To help fund retirement in a world of low interest rates, retirees increasingly have to tolerate some level of risk in their portfolios – adding to the volatility of returns. Combine volatility with the need to make regular withdrawals, and retirees are especially at risk of prematurely depleting their capital should a savage market downturn take place early in their retirement years. This scenario highlights the potential benefits of a risk management overlay.

Time is not a luxury retirees can afford

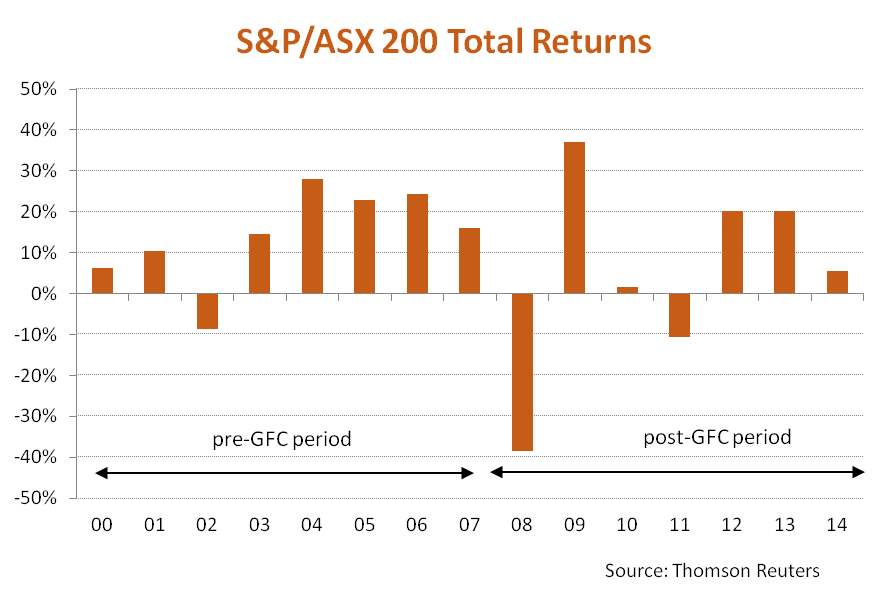

Most investors are familiar with the saying: ‘Time in the market, not timing the market’. It correctly highlights the importance of long-term investing however it fails those retirees who are likely to bear greater losses than other investors when market downturns strike early. The key risk occurs when an investor switches from accumulating wealth to drawing it down – a moment when balances are usually at their highest. This key risk factor, also known as ‘sequencing risk’, can prove toxic to the quality of retirement because retirees have to withdraw from their portfolios whether the market is up or down. If a downturn strikes early in retirement retirees can end up locking in substantial capital losses which are unlikely to ever be recouped, forcing them to reduce withdrawals or risk running out of retirement savings far earlier than planned. As an illustration, assume an investor has a portfolio worth $400,000 at 1 January 2000, which is fully invested in the S&P/ASX 200 Index. If left untouched, the portfolio would be worth $1.3 million by the end of 2014, due to a compound annual return from the market of 8.2 per cent. However, if we reversed the sequence of returns – starting with the weak post-GFC period (2007-2014), followed by the stronger 2000-2007 period – the compound annual returns would still be 8.2 per cent over this period, and the investor would still be left with $1.3 million.

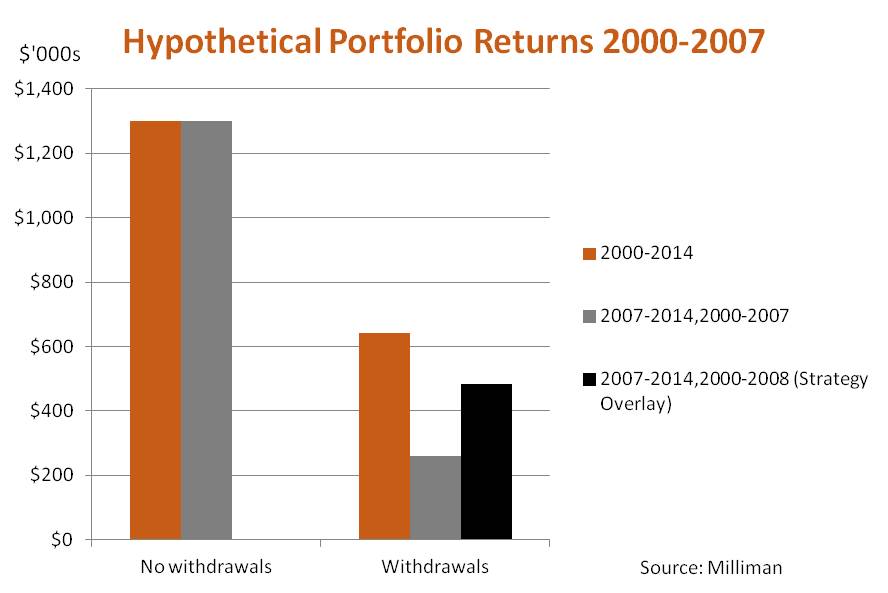

When no withdrawals take place, the order or “sequencing” of returns over a given time period does not matter. Now assume, however, the investor is also a retiree – and they draw down their savings on a monthly basis starting with an amount of $1,667 which is equivalent to a rate of 5 per cent per annum of the initial balance. The monthly withdrawal is also indexed to the realised month on month inflation. By the end of 2014, the portfolio would be worth $642,000 – despite the withdrawals – due to the returns of the market over this period. However, if we then reverse the returns – with the weak post-GFC period coming ahead of the stronger pre-GFC period, the portfolio by the end of 2014 would now only be worth $261,000. It underscores the high level of variability of returns for those in withdrawal phase. This impact on retirement withdrawals caused by a significant drop in portfolio value early in retirement is known as “sequencing risk”.

Risk management overlay

One way to help manage sequencing risk is to apply a dynamic risk exposure strategy, which seeks to reduce downside market risk. As an illustration, if we add Milliman’s risk management overlay, which has been used by some of the world’s largest insurance companies since the 1990s, the portfolio would hypothetically have ended the period with $482,000, rather than just $261,000.

Illustration only. Past performance, actual or hypothetical, is not an indication of future performance. BetaShares combined its expertise with Milliman to launch the BetaShares Australian Dividend Harvester Fund (managed fund) last November. The fund invests in large-cap Australian shares with the objective of delivering franked income that is at least double the yield of the Australian broad sharemarket while reducing volatility and managing downside risk.

This article was first published in BetaShares Blog.