Investors know that growth assets such as shares and property typically deliver strong long-term returns. What they don’t know is that the long-term may be much longer than they’re prepared for and the risks on the journey far greater than imagined.

While there is a strong correlation between risk and return, there are often long periods of time when investors aren’t rewarded for taking on greater risk.

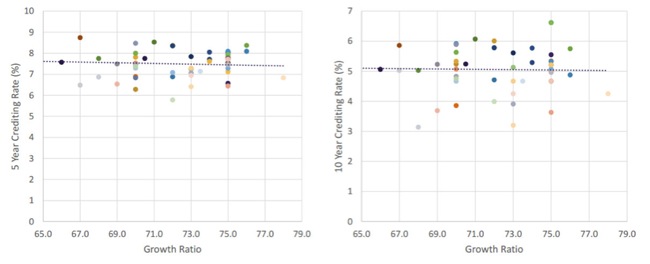

Super funds which made higher allocations to growth assets (in the range of 66% to 78%) failed to see higher returns in their balanced portfolios over the five- and 10-year periods ended March 2016, according to a recent analysis by asset consultant Frontier Advisors and SuperRatings.

Figure 1: A higher growth ratio has not proved to be a key factor in driving returns

| Growth asset ratio versus 5 year returns to March 2016 | Growth asset ratio versus 10 years returns to March 2016 |

|

|

| Source: SuperRatings | |

The result is all the more surprising given that super funds employ a range of sophisticated investing techniques and have the flexibility to shift their portfolios to take advantage of market fluctuations.

A number of single growth asset classes display similar periods where growth (but not risk) is severely lacking.

Japan’s late-80s asset price bubble led its economy into a lost decade and its share market stagnated for much of it. While many emerging markets have posted periods of strong economic growth, there are long periods where it has not translated into equity market gains. The MSCI Emerging Markets Index (USD) lost an average 3.78% a year over the five years to June 30, 2016, and gained just 3.54% a year over the decade (with significantly more volatility and risk than most developed markets).

Such comparatively weak results from growth assets can even be seen in the Australian share market.

Australian shares delivered a gross average annualised return of 5.5% over the decade ended 2015, outpaced by a conservative managed fund (5.6% return) and a balanced fund (5.7% return), according to the latest Russell Investments/ASX Long-term Investing Report.

It all comes down to timing. Without a true appreciation of volatility, even long-term return averages can be highly misleading.

The true risks can be summed up in a Drew, Walk & Co study (sponsored by Challenger), which analysed equity market returns since 1900 across 21 countries. It found an approximate one-in-five chance that 20-year historical equity returns would be lower than the risk-free return.

What is the long-term?

Such episodes of long-term underperformance are cause for concern. Outside of superannuation, few investors hold their investments for more than a decade.

Even within the super environment, investors facing another 20 years of mandatory contributions – typically those around 45 years of age – have far less time to recover from market downturns. Those already retired and drawing down a pension may never recover.

Still, few investors plan that far ahead.

Around one-quarter of Australians surveyed by the corporate regulator's Australian Financial Attitudes and Behaviour Tracker said they held 15- to 20-year financial plans.

A more troubling finding was that the proportion of those long-term investors who said they “had kept an investing rule or strategy they’d set” fell to 42% – down from 57% just 18 months earlier.

When market conditions become treacherous, the behaviour of investors becomes increasingly self-defeating. They tend to fall into traps such as loss aversion and other behavioural biases.

A separate survey recently highlighted another mismatch between the length of time that investors hold their portfolios and their return expectations.

Just one-quarter of Australian investors said they held their investments for at least five years, according to the latest Schroders Global Investor Study – and yet almost half (45%) of investors wanted a yield of at least 10%.

It may seem fanciful given the fallout from the 2008 global financial crisis continues almost a decade later: global growth remains tepid, debt continues to mount and interest rates remain near historic lows in many parts of the world.

The disconnect can be measured in excess risk: volatility and the potential for capital losses.

A new perspective on risk

There is no doubt that investors need higher returns to fund longer retirements in a low-inflation environment which has curtailed returns of traditional “safe” assets.

But “buy-and-hold” or “set-and-forget” strategies are clearly not an adequate safeguard against risk. Neither is chopping and changing investments in the face of volatile market conditions given widespread behavioural biases and the generally poor results generated by trying to time markets.

Investors need risk management that extends beyond the traditional safeguards of a long-term perspective and diversification. Both are important investment tenants, but there is now a weight of evidence to show that being wholly reliant on them will leave many investors still exposed to excessive risks and, in many cases, disappointment.

A more sophisticated approach to risk management should be holistic and flexible enough to accept the behavioural shortcomings of investors. In many cases, this will mean leaving some returns on the table in return for less volatility and greater certainty.

Advances in technology now allow advisers to genuinely assess the risk that investors won’t achieve their goals by running real-time simulations incorporating thousands of potential market scenarios. They can then decide which actions they need to take to reach them.

These actions can be paired with a range of more sophisticated investment techniques originally used in the institutional sector, including dynamic exposure management strategies, to specifically manage risk.

Growth assets play to important a role in investors’ portfolios to leave the outcome to a “long-term” which may never arrive.

Disclaimer

This document has been prepared by Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives, [and for other persons who are wholesale clients under section 761G of the Corporations Act].

To the extent that this document may contain financial product advice, it is general advice only as it does not take into account the objectives, financial situation or needs of any particular person. Further, any such general advice does not relate to any particular financial product and is not intended to influence any person in making a decision in relation to a particular financial product. No remuneration (including a commission) or other benefit is received by Milliman AU or its associates in relation to any advice in this document apart from that which it would receive without giving such advice. No recommendation, opinion, offer, solicitation or advertisement to buy or sell any financial products or acquire any services of the type referred to or to adopt any particular investment strategy is made in this document to any person.

The information in relation to the types of financial products or services referred to in this document reflects the opinions of Milliman AU at the time the information is prepared and may not be representative of the views of Milliman, Inc., Milliman Financial Risk Management LLC, or any other company in the Milliman group (Milliman group). If AFS licensees or their representatives give any advice to their clients based on the information in this document they must take full responsibility for that advice having satisfied themselves as to the accuracy of the information and opinions expressed and must not expressly or impliedly attribute the advice or any part of it to Milliman AU or any other company in the Milliman group. Further, any person making an investment decision taking into account the information in this document must satisfy themselves as to the accuracy of the information and opinions expressed. Many of the types of products and services described or referred to in this document involve significant risks and may not be suitable for all investors. No advice in relation to products or services of the type referred to should be given or any decision made or transaction entered into based on the information in this document. Any disclosure document for particular financial products should be obtained from the provider of those products and read and all relevant risks must be fully understood and an independent determination made, after obtaining any required professional advice, that such financial products, services or transactions are appropriate having regard to the investor's objectives, financial situation or needs.

All investment involves risks. Any discussion of risks contained in this document with respect to any type of product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved.