Defined benefit (DB) super funds, which effectively guaranteed employees’ final retirement payouts decades in advance, had their heyday in the 1980s and 90s.

For those still lucky enough to be in one, it has been a blessing. For employers and public bodies tasked with funding them, it has been anything but as market gyrations and rising lifespans have made meeting those liabilities increasingly difficult.

The majority of employees may now be in defined contribution plans (they have sole responsibility to ensure they don’t run out of money in retirement), but thousands of Australians remain in DB schemes, which owe them a sizeable $342 billion.

Markets over the last five years have turbocharged all funds, but before then, many DB schemes were on far shakier ground.

An Australian Securities and Investments Commission (ASIC) review of approximately 470 DB funds released in January 2013 found that more than one-third (38%) had a vested benefits index (VBI) of less than 100%.1 The VBI is an estimate of total benefits owed to all members if they voluntarily left their employer on the same date (another common measure is the accrued benefit index).

This means a substantial proportion of DB funds were not in a “strong financial position”, even after markets rebounded from the global financial crisis (GFC) , based on the Australian Prudential Regulation Authority’s (APRA) guidance.

While the majority of those funds will now be fully funded, the VBI measure still obscures the risk inherent in DB funds. While a VBI that is positive (or even above a predefined threshold) may be considered “well funded”, it is a point in time measure that doesn’t reflect the underlying risk.

This is because trustees are managing a convex liability: when returns are exceptional, members typically retain the upside, as is the case with defined benefit “underpin” schemes. But when returns are poor, the downside to DB fund trustees can be unlimited.

Many DB funds are still strongly exposed to similar levels of growth assets and market risk as defined contribution funds. This has been a benefit in recent years but it can equally drag down funds when markets inevitably turn down.

Surplus DB assets are also typically invested in the same asset classes as accumulation assets. This means excess funding won’t offer much of a buffer when markets are stressed – these surplus assets will decline in value as fast as the rest of the fund.

The outcome could be a repeat of the post-GFC disaster. While some DB funds may have legal avenues to reduce member benefits or seek top ups from employers, going down these paths again is undesirable for obvious reasons.

Case study

Milliman worked with a client concerned about its defined benefit liability. This was a legacy multi-employer arrangement under which members retained accumulation balances in addition to a defined benefit “underpin” which essentially guarantees a minimum accumulation balance at retirement.

While this fund was well funded from a regulatory point of view and able to meet forecasted liabilities under best estimate assumptions about long-term asset returns, the fund recognised the potential for insolvency in the event of a market crash. This particular client had previously investigated asset allocation strategies and investment bank solutions to manage the DB liability. However, the options were either expensive or didn’t recognise the uncertain nature of member behaviour.

Milliman worked with this client to assess the situation and proposed a dynamic hedge strategy using liquid, exchanged traded futures. The cost of running this hedge strategy is funded by reserves and is expected to allow the fund to meet its liabilities in a wide range of market scenarios.

Milliman continuously monitors the scheme’s defined benefit liability and adjusts hedge positions as markets move and based on member behaviour.

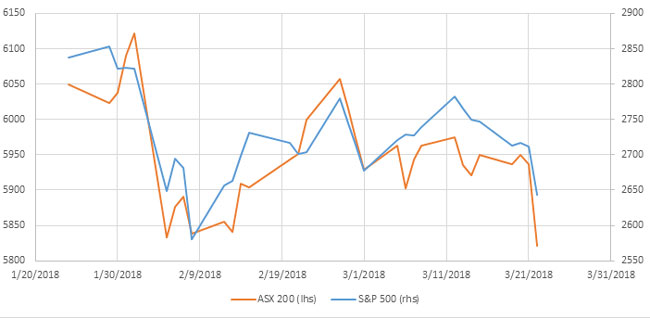

During the recent period where US equities fell almost 7% from their January peak and Australian equities fell 4%, this particular client experienced a 10% increase in its DB surplus. Contrast this with the expected performance of typical DB funds where surplus assets are invested in the same risky growth assets as accumulation balances.

Figure 1: Recent market performance

Conclusion

Australia has been fortunate to experience 25 years without a recession. The ASX trades near historic highs and we have experienced a historic bull run in fixed income. As we near the 10-year anniversary of the GFC, recent equity market corrections reminds us of the inherent risks of investing.

Home insurance is best purchased well before the fire brigade arrives. Similarly, DB funds should seize the opportunity to revisit the nature of their liabilities and strategies to manage them while times are good.

It’s not a crisis if you see it coming.

1 http://asic.gov.au/about-asic/media-centre/find-a-media-release/2013-releases/13-004mr-asic-encourages-good-disclosure-from-defined-benefit-fund-trustees/

Disclaimer

This document has been prepared by Milliman Pty Ltd ABN 51 093 828 418 AFSL 340679 (Milliman AU) for provision to Australian financial services (AFS) licensees and their representatives, [and for other persons who are wholesale clients under section 761G of the Corporations Act].

To the extent that this document may contain financial product advice, it is general advice only as it does not take into account the objectives, financial situation or needs of any particular person. Further, any such general advice does not relate to any particular financial product and is not intended to influence any person in making a decision in relation to a particular financial product. No remuneration (including a commission) or other benefit is received by Milliman AU or its associates in relation to any advice in this document apart from that which it would receive without giving such advice. No recommendation, opinion, offer, solicitation or advertisement to buy or sell any financial products or acquire any services of the type referred to or to adopt any particular investment strategy is made in this document to any person.

The information in relation to the types of financial products or services referred to in this document reflects the opinions of Milliman AU at the time the information is prepared and may not be representative of the views of Milliman, Inc., Milliman Financial Risk Management LLC, or any other company in the Milliman group (Milliman group). If AFS licensees or their representatives give any advice to their clients based on the information in this document they must take full responsibility for that advice having satisfied themselves as to the accuracy of the information and opinions expressed and must not expressly or impliedly attribute the advice or any part of it to Milliman AU or any other company in the Milliman group. Further, any person making an investment decision taking into account the information in this document must satisfy themselves as to the accuracy of the information and opinions expressed. Many of the types of products and services described or referred to in this document involve significant risks and may not be suitable for all investors. No advice in relation to products or services of the type referred to should be given or any decision made or transaction entered into based on the information in this document. Any disclosure document for particular financial products should be obtained from the provider of those products and read and all relevant risks must be fully understood and an independent determination made, after obtaining any required professional advice, that such financial products, services or transactions are appropriate having regard to the investor's objectives, financial situation or needs.

All investment involves risks. Any discussion of risks contained in this document with respect to any type of product or service should not be considered to be a disclosure of all risks or a complete discussion of the risks involved. Investing in foreign securities is subject to greater risks including: currency fluctuation, economic conditions, and different governmental and accounting standards. There are also risks associated with futures contracts. Futures contract positions may not provide an effective hedge because changes in futures contract prices may not track those of the securities they are intended to hedge. Futures create leverage, which can magnify the potential for gain or loss and, therefore, amplify the effects of market, which can significantly impact performance.

An investment in an underlying portfolio, whether with or without Milliman Managed Risk Strategy (MMRS) is subject to market and other risks and no guarantee or assurance is given by Milliman AU or any company in the Milliman group that the use of MMRS in connection with an underlying portfolio will not give rise to losses or that the performance of the MMRS in relation to the underlying portfolio will remove volatility completely or to the extent depicted in an illustration or fully replace losses in the underlying portfolio or to the extent depicted. While generally assets used in connection with the MMRS are liquid, this may not be the case in all circumstances. Further, during periods of sustained market growth, the return to clients from the combination of an underlying portfolio and MMRS should be less than if a client had no MMRS.

Any source material included in this document has been sourced from providers that Milliman AU believe to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by any company in the Milliman group as to the accuracy or completeness of the source material or any other information in this document.

Past performance information provided in this document is not indicative of future results and the illustrations are not intended to project or predict future investment returns.

Any index performance information is for illustrative purposes only, does not represent the performance of any actual investment or portfolio. It is not possible to invest directly in an index.